Last year I wrote an article (“Operation Choke Point”), which detailed how the federal government has weaponized the US banking system to deny access to political foes and disfavored industries like cannabis, firearms manufacturing or crypto. The article was in response to one of the most egregious abuses of power in American history, where government regulators shut down almost every American bank that supported the crypto industry - including at least one that was solvent at the time.1

More recently, OCP has once again made headlines as the public begins to grasp the magnitude of how the Biden Administration has used government power to weaponize the US banking system - not just against industries, but even its political foes and their businesses.

The sparks started to fly last week when venture capitalist Marc Andreessen appeared on the Joe Rogan podcast, and disclosed that White House officials had told him “not to bother” starting new companies in chosen fields where the government wanted to exercise control, such as artificial intelligence.2

These officials knew that they couldn’t overtly move against private companies, so they outsourced the dirty work to the heavily regulated banking system - whose managers readily shut down bank accounts of targeted individuals and businesses without explanation.

This practice of lawfare and politically-motivated de-banking is deeply un-American and clearly illegal. But as much as we would like to write off Operation Choke Point as an isolated incident, US federal bureaucrats have been using coercion and implied threats to shut down businesses that they oppose on ideological grounds - in many industries.

The struggling health insurance market is no exception. As if the industry doesn’t already have enough problems, we now know that officials in the Obama and Biden administrations have used their regulatory power to deny choice to the American consumer.

Health insurance has its own ‘choke point’

The public is rightly focused on allegations of government overreach against technology startup founders - but for most of the past decade federal bureaucrats have exercised similar abuses of power in the health insurance sector.

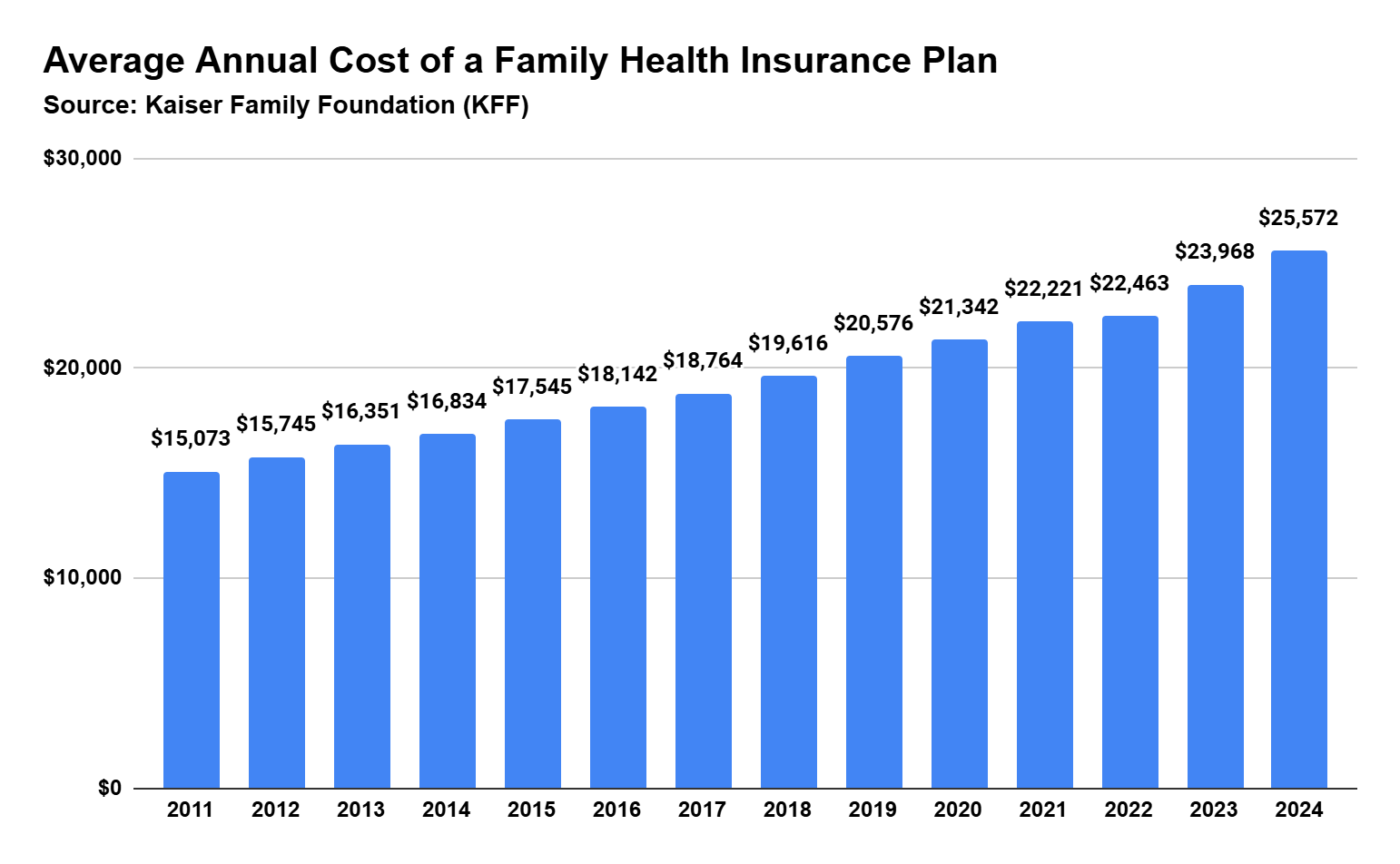

Congress passed the Affordable Care Act (the “ACA”; informally known as “Obamacare”) into law in 2010. Like many government laws, the ACA is ironically named since its impact has led to costs that are anything but affordable - as the below chart demonstrates.

Among the many challenges that middle-class Americans face these days, nothing is more insidious than the skyrocketing cost of health insurance. The average cost of a family plan rose 6.6% last year3 – more than double the rate of inflation according to the Bureau of Labor Statistics (BLS).4

Currently we are in the middle of ‘open enrollment’ season, where the government ‘allows’ people to choose which low-quality Obamacare HMO they will use in the coming year. The increase in costs for those plans will rise by a nationwide average of 7% in 2025, or more than double the official rate of inflation. Meanwhile, the maximum out-of-pocket cost for any family on Obamacare will rise to an eye-watering $9,200 for an individual — or $18,400 for a family.5

These costs are already unsustainable for many people, and we are hurtling toward a reality where almost no one can afford Obamacare. We are, in fact, already there since the US government subsidizes insurance costs for lower-income families.

How much does that subsidy cost? The Congressional Budget Office (CBO), a non-partisan government agency, announced that federal Obamacare subsidies cost the taxpayer $125 billion last year – and they forecast that amount will rise to a whopping $3.3 TRILLION by 2033. In case you’re wondering, that will amount to over 10% of our current GDP.6

Any program that requires trillions of dollars in ‘subsidies’ is clearly broken. And yet rising premiums are only part of the problem.

Obamacare deductibles are also rising, as are the feared “maximum out-of-pocket” amounts that an insured person must pay before their insurer covers all costs. How many Americans can actually afford to pay over $9,000 if one of their loved ones experiences a health emergency?

My social media feed is full of comments like this:

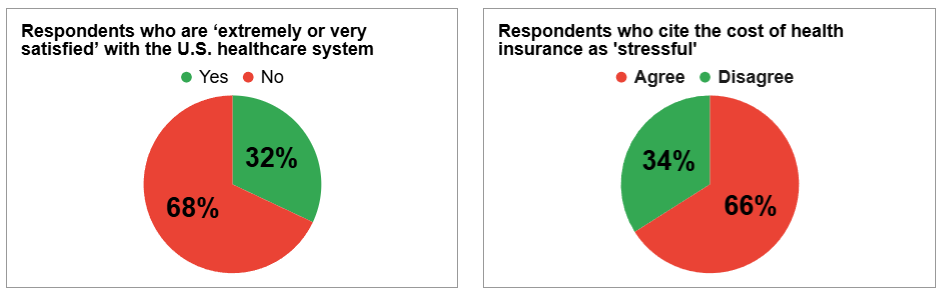

These high costs would at least be understandable if people were satisfied with their coverage. Yet we are rapidly approaching the point where a majority of working-age Americans are unhappy with their health insurance, and with the entire healthcare industry.7

Health insurance costs have become a major source of stress at every income level, but particularly for middle-class families. Yet the story goes largely unreported, beyond the occasional human-interest story or data-driven WSJ article.

When tens of millions of Americans mention health insurance as a significant source of stress in their lives, it seems natural that companies would see an opportunity to provide a superior alternative to the market.

And in fact, there are better alternatives. Top-tier insurance carriers like Allstate and UnitedHealthCare offer health insurance plans that are not regulated by the ACA and offer more comprehensive coverage at lower cost - in many cases less than half the cost of a comparable Obamacare plan.

Such plans are often referred to as “short-term limited duration insurance” (STDLI, also known as “short-term medical”). We refer to them as “free-market plans” since the insured does not require government assistance or an employer to qualify.

Congress exempted these plans from federal health insurance regulations in 1996 so that carriers could provide affordable, comprehensive coverage to people who find government-regulated options to be affordable (which today includes tens of millions of American taxpayers). As the name suggests, these plans could only be issued for a maximum of twelve months - but they were a viable and affordable alternative, and could be renewed.

The CBO - a government agency! - has published findings that demonstrate the superiority of free-market plans when compared to Obamacare:8

- The CBO has found that 95 percent of STLDI plans are a “comprehensive major medical policy.”

- STLDI “may exclude some benefits that [Obamacare] plans must cover [but] may have lower deductibles or wider provider networks” than Obamacare plans.

- The CBO finds that for many consumers, comprehensive STLDI carries premiums that are “as much as 60 percent lower than premiums for the lowest-cost bronze [Obamacare] plan.”

Given the obvious appeal of free-market health insurance, consumers should be outraged that politicians and bureaucrats are openly hostile to these plans. Instead, the political establishment has been working tirelessly to limit consumer choice and to shut down affordable alternatives to the so-called Affordable Care Act - even with its low-quality coverage and crushing burden on the US taxpayer.

Short-term plans operated in parallel to Obamacare until 2016, when the outgoing Obama administration issued an executive order that reduced the maximum duration of free-market plans from twelve months to three.9 This effectively closed down the free market option until 2018, when President Trump issued his own order to extend the maximum duration of a free-market policy to 36 months.10

Trump’s order remained in effect until September 2024, when the outgoing Biden administration countermanded Trump’s executive order and - once again - limited short-term plans to no more than three months’ duration - and now the government is prohibiting renewals.11

How and why the government works against free-market health insurance

As we have already seen, the US health insurance system is utterly broken and costs are unaffordable - not just for many middle-class families, but for the government itself. So then, why is the federal government blocking free-market alternatives that could help families to save thousands of dollars per year - and receive better coverage?

Michael Cannon from the libertarian-leaning CATO Institute offers great perspective here:12

“The Departments claim their objective is to protect patients with preexisting conditions and to protect consumers from low-quality coverage. Yet the rule they have proposed would do the exact opposite. Longer contract periods and renewals increase health plan quality by increasing enrollees’ ability to pool their medical expenses with others and by enabling continuous coverage. By prohibiting these features, the Departments would be requiring STLDI issuers to offer lower-quality coverage.

The Departments are fully aware that they are…mandating low-quality coverage. They acknowledge that their proposal would take coverage away from sick patients, could increase overall the number of uninsured, and would therefore expose STLDI enrollees to “an increased risk of higher out-of-pocket expenses and medical debt, reduced access to health care, and potentially worse health outcomes.” They acknowledge that their proposal is so dangerous it requires a warning label.

The fact that the Departments nevertheless issued this proposal indicates their goal is not to protect patients but to protect Obamacare, even at the cost of harming patients. Their objection to STLDI is not that it is low-quality but that it is of sufficiently high quality that millions of consumers are choosing it as a reasonable alternative to Obamacare. STLDI is too good, so the Departments are trying to make it bad. It is too comprehensive, so the Departments want to make it less comprehensive. The NPRM reveals the Departments’ actual purpose is to boost Obamacare enrollment by punishing consumers who make what the Departments—not Congress—believe to be the “wrong” choice.”

Millions of Americans don’t qualify for employer-sponsored insurance and are forced to pay thousands of dollars a month for Obamacare plans that become more expensive with every passing year, even as the quality of coverage deteriorates. Why on earth would our government want to take a viable option off the table when it could help millions of people?

One of Obamacare’s staunchest defenders is the Commonwealth Fund, a left-wing healthcare advocacy group that bills itself as an “antiracist organization” and seeks complete government control over the healthcare market.13 Their website notes the federal bureaucracy’s recent move to shut down free-market health insurance and states the following - without a trace of irony:14

“While appealing to some healthy individuals, [free-market plans] are often unattractive, or unavailable, to people in less-than-perfect health. By leveraging their regulatory advantages to enroll healthy individuals, these alternatives to marketplace coverage may contribute to a smaller, sicker, and less stable ACA-compliant market. Recent testimony proves that they’re willing to shut down free-market alternatives, even if it means some consumers will suffer—in the administration’s words—“potentially worse health outcomes.”

The primary difference between a capitalist and a communist is that capitalists advocate for “equality of opportunity” while communists support “equality of outcomes”. When adopted as government policy, the latter is guaranteed to crush innovation and drive society’s most productive individuals out of the market. Why should anyone work hard when the government will just confiscate their wealth and “re-distribute” it to their lazy neighbor down the street?

Yet that is exactly what the Commonwealth Fund and its cronies in our federal bureaucracy are fighting for. As far as they are concerned, the fact that you are healthy should not entitle you to better and more affordable opportunities than someone who is less healthy. They are advocating for equal outcomes – a deeply damaging idea that is directly at odds with the principles of free enterprise and American capitalism.

Why We Support Free-Market Health Insurance Options

Federal bureaucrats have no problem with auto insurers offering better rates to good drivers, or refusing to extend offers of coverage to bad drivers. Similarly, Coverbook believes that insurers should be free to offer preferential coverage and rates to healthy people. This practice creates significant economic incentives for the insured individual to maintain a healthy lifestyle. Doing so also brings the added benefit of reducing that person’s reliance on government, and reducing the burden that they place upon the government. It is a virtuous cycle that, when deployed at scale, can ultimately resolve our nation’s healthcare crisis.

We expect that, in the coming months, the incoming Trump administration will once again reverse Biden’s misguided executive order and reinstate the market for short-term health insurance. In the meantime, we are able to offer short-term options with a coverage limit of three months to anyone who may need it.

We can also offer fixed indemnity health insurance plans that make a cash payment to the insured whenever they experience a covered event, like a hospitalization or a routine child’s visit to an urgent care clinic. Government bureaucrats force fixed indemnity carriers to provide a disclaimer that states these plans “are not health insurance under the ACA”. While this may be true in a narrow sense, fixed indemnity plans are still very useful coverage that protect against the worst-case scenario - and provide the insured with far greater coverage than most Obamacare HMOs. We recommend you read more about fixed indemnity plans here.

We believe that government should work for the people. A critical role for politicians and regulators is to advocate for consumer choice, and to ensure that taxpayers have the best possible options and consumer protections available. We intend to be a relentless advocate for consumer choice in affordable health insurance, and encourage all who are interested to follow us.

About Coverbrook

Coverbrook is an independent insurance agency that works with America’s largest insurers to provide access to ‘free-market’ health insurance plans outside of the government marketplace or employer-sponsored plans. Our mission is to help individuals to become more self-reliant by promoting health insurance options that save money and help our clients to protect against the unexpected, while prioritizing individual freedom.

Subscribed

1 https://nymag.com/intelligencer/2023/03/barney-frank-says-more-shuttering-signature-bank.html

2 YouTube, “Joe Rogan Experience #2234 - Marc Andreessen”. Censorship content starts at 2:36:46.

3 https://files.kff.org/attachment/Employer-Health-Benefits-Survey-2024-Annual-Survey.pdf

4 https://www.usinflationcalculator.com/inflation/consumer-price-index-and-annual-percent-changes-from-1913-to-2008/

5 https://www.cms.gov/files/document/2025-papi-parameters-guidance-2023-11-15.pdf

6 https://budget.house.gov/download/-president-of-paragon-institute-reviews-cbo-annual-report-of-federal-health-insurance-subsides_highlights-need-for-change-of-direction-in-health-policy#:~:text=%E2%80%9CAccording%20to%20the%20CBO%2C%20federal,percent%20of%20GDP%2C%20respectively.%E2%80%9D

7 https://www.ipsos.com/en-us/mdvipipsos-poll-shows-americans-are-struggling-healthcare-system

8 https://www.govinfo.gov/content/pkg/FR-2023-07-12/pdf/2023-14238.pdf

9 https://www.kff.org/affordable-care-act/issue-brief/understanding-short-term-limited-duration-health-insurance/

10 https://www.cms.gov/newsroom/press-releases/hhs-news-release-trump-administration-delivers-promise-more-affordable-health-insurance-options

11 https://nationalhealthcouncil.org/blog/biden-administration-addresses-short-term-health-plans/

12 https://www.cato.org/policy-analysis/biden-short-term-health-plans-rule-creates-gaps-coverage

13 https://www.commonwealthfund.org/about-us

14 https://www.commonwealthfund.org/publications/fund-reports/2018/mar/state-regulation-coverage-options-outside-affordable-care-act